Realtor.com® National Housing Forecast Update 2022: A Moderating Housing Market Means More Options for Home Shoppers

- Mortgage rates have been revised upward to reflect the major shift in monetary policy and financial conditions over the last 6 months; in the second half of 2022, we expect a continued climb at a more modest pace, which means that rates hit 5.5% by year-end

- Going forward, home price growth cools, but it has remained hotter for longer than originally anticipated leading to an upwardly revised projection of 6.6% home price growth for 2022

- Home sales slow, shifting our original 2022 growth expectations to a decline of 6.7%. While we now forecast a notable step down from 2021, home sales on par with these projections would mean that 2022 sales are the 2nd highest tally since 2007, trailing only 2021.

- The number of homes for sale grows more than originally projected. The growth is driven by a combination of more sellers and a slowing home sales pace.

Realtor.com® 2022 Forecast for Key Housing Indicators

| Housing Indicator | 2022 Realtor.com® Forecast Update | 2022 Realtor.com® Forecast | ||

| Existing Home Median Sales Price Appreciation | Up 6.6% | Up 2.9% | ||

| Existing Home Sales | Down 6.7% | Up 6.6% | ||

| Existing Home For-Sale Inventory | Up 15% | Up 0.3% | ||

| Mortgage Rates | Average 5% throughout the year, 5.5% by end of year | Average 3.3% throughout the year, 3.6% by end of year | ||

| Single-Family Home Housing Starts | Up 5% | Up 5% | ||

| Homeownership Rate | 65.6% | 65.8% |

A Changing Economic Landscape

Inflation is High and Monetary Policy Pivots

The change in financial conditions is the most dramatic driver of change in our revised outlook. As we finalized our results in late 2021, the consensus on inflation being a largely transitory phenomenon that could be tamed with a garden-variety tightening cycle was just starting to crack as inflation accelerated from just over 5% in August to more than 7% by December. In the December 2021 Fed meeting, decision makers accelerated the planned end date of the Fed’s asset purchase program and raised expectations for short term rates by the end of 2022 to just shy of 1%, which would imply roughly three quarter point rate hikes in 2022. In its January 2022 meeting, the Fed signaled their plan to begin rate hikes at the March 2022 meeting, and markets responded. In the span of roughly two months, futures markets had re-priced a March hike from a longshot to near certainty.

The Fed followed through in March, and in addition to lifting the Fed funds rate, their economic projections signaled that more and/or larger rate hikes would be needed than expected in December. At its recent May meeting, the Fed made good on those expectations, raising the short-term rate by 50 basis points, the biggest hike in 22 years, and setting the groundwork for more large adjustments. Because inflation does not respond immediately to tighter monetary conditions, it has continued to surge, hitting 8.6% in March before easing somewhat to 8.2% in April. We expect that inflation will continue to ease as demand responds to tighter financial conditions, but remain high enough to pressure the Fed to continue moving short term rates rapidly to neutral. Once we hit a growth- and inflation-neutral short-term rate, likely in late 2022, we expect the Fed to pause and assess the impact of its actions on the economy before deciding whether to hold or pursue additional hikes. Mortgage rates will likely continue to climb, but at a slower pace, as they’ve largely adjusted to anticipate the Fed’s hikes through the end of 2022.

In December 2021, our call of 3.6% mortgage rates in 2022 was on the higher end of expectations. Now, however, mortgage rates have already exceeded 5% for over a month. This shift is reverberating through the housing market and consumer decisions. Mortgage rates are currently more than 2 percentage points higher than this time one year ago. In combination with higher home prices, this has caused monthly mortgage payments to soar, by more than 50% relative to one year ago. For a home buyer financing 80% of the typical home purchase price, this is roughly an extra $600 per month. While higher costs have dampened homebuyer demand, knocking some households out of the hunt for a home entirely, consumers expect mortgage rates to continue to climb. This means that home shoppers who continue to search, will feel a strong sense of urgency to act quickly in the hopes that they may secure a lower rate.

Employment and Income Remain High, Supporting Demand Despite Tighter Financial Conditions

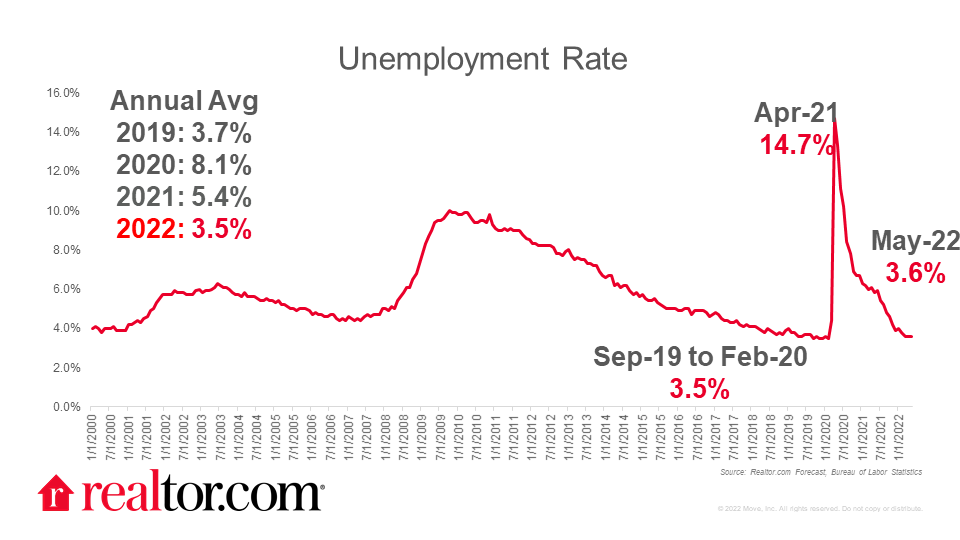

While the number of jobs in the economy has yet to reach its pre-pandemic high mark, it is rapidly nearing that threshold. Meanwhile, the pandemic’s lingering drag on labor force participation and a strong economy driving demand for labor have pushed the unemployment rate down to just above its pre-pandemic 50+ year low, putting upward pressure on wages as firms compete to attract and retain workers. We expect these conditions to persist through the end of the calendar year with the unemployment rate averaging 3.5% and wages growing by an upwardly revised 3.8%. Although wages do not keep up with inflation, they continue to grow at above-average rates and the sense that jobs are plentiful boosts consumer confidence and enables workers to change jobs at higher rates than in the past. And while workers return to offices in greater numbers, increased workplace flexibility is expected to be one lasting legacy of the pandemic, weakening the tie between job centers and housing, and enabling some home searchers to circumvent higher housing costs by relocating.

Economic Growth (Gross Domestic Product) Slows as Crisis-Era Fiscal Stimulus Fades and Global Uncertainties Weigh

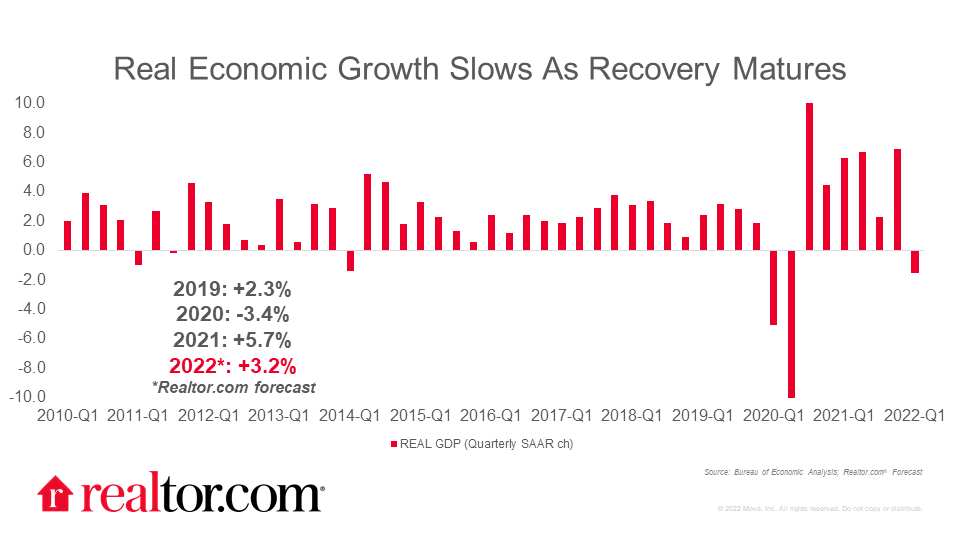

Forecast GDP declined between our end of year forecast and updated inputs now as inflation and tighter financial conditions each take a larger and larger chunk out of real growth. Real GDP growth was revised from +4.3% in 2022 to +3.2%, so current inputs suggest that the economy continues to see nearly trend-level growth in 2022. However, risks to this projection remain. First, as pandemic aid winds down, fiscal policy becomes a mathematical drag on overall growth, and in fact, the first quarter of 2022 saw weaker GDP growth largely because of a decline in private inventory investment and a pull back in government spending. Second, even though the Fed is pursuing a soft landing, tighter financial conditions will weigh on growth as consumers and businesses alike face higher borrowing costs. Third, the war in Ukraine–begun more than 3 months ago–and ongoing economic disruptions from China’s COVID policies are also risks as they are likely to disrupt supply chains and feed into general uncertainty, consumer unease, and additional price increases.

Key 2022 Housing Trends

State of Housing – The Market Settles Down as Home Sales Moderate, and Price Growth Eases

Over the last couple of years the housing market has experienced significant ups and downs. Substantial pre-COVID sales momentum was brought to a halt early in the pandemic only to be unleashed as the economy reopened. Home sales activity hit long-term highs unseasonably late in 2020 as consumers tried to make up for a largely lost spring season and capitalize on falling mortgage rates. The momentum carried into 2021, waning a bit in the peak spring and summer season before reemerging later in the year as concerns over rising mortgage rates emerged causing buyers contemplating a move to hurry-up and beat rising rates.

In 2022 we witnessed the early year housing frenzy give way to tough budget realities as rates hit decade-plus highs and home prices continued to surge, causing some buyers to postpone home buying plans in the face of higher costs. Home sales activity finished 2021 and started 2022 off better than previously expected, but cost challenges have caused us to revise our outlook for home sales down lower. We now expect home sales to slip 6.7% in 2022. We expect to see the biggest year over year weakness in home sales in what’s traditionally the heart of the summer selling season. As we move into cooler months and both buyers and sellers have an opportunity to recalibrate their expectations of the housing market, we expect to see somewhat greater transaction activity, but sales will still lag year-ago pace. As conditions shift, we expect home purchases by investors to slip by a relatively small amount while homebuyer purchases for both primary and secondary homes decline by a larger amount. This causes the share of purchases by non-occupiers to grow while the share of homes purchased by owner-occupiers declines, which puts pressure on the homeownership rate.

Builders Ramp Up to Tackle Housing Undersupply

Construction remains sorely needed in a housing market that is still undersupplied. The government has taken note, with the White House rolling out a plan to tackle the housing shortage, primarily by making it easier to permit and fund smaller, more affordable homes, which is expected to lead to more construction of these dwellings. Much like overall sales activity, single-family housing starts finished slightly stronger than expected in 2021 and are poised to build on that momentum in 2022. We expect single-family housing starts to hit a new 16-year high in 2022, but rising costs and labor shortages will present challenges for builders to work around on top of waning optimism and top-line pressures as housing demand softens.

Home Buyers See the Number of Options Improve, but Costs Remain High for Both Buyers and Renters

Our forecast revisions highlight challenges and opportunities for buyers. While housing costs remain high, pushing home shoppers to make tough choices about their budget priorities, the number of homes for sale is expected to continue to grow, building on the turnaround begun in May. As more homeowners look to make adjustments to fit changing personal needs and take advantage of favorable market conditions to access the significant amount of equity they have likely accumulated, home shoppers will have more choices. This may even lead to a reinforcing cycle, as more options bring out other seller-buyers–those hoping to both sell a home and buy another at the same time. For those households who simply can’t keep up with the rising cost of home buying, renting may be the better option. But for other renters, especially the large number of millennials near prime first-time home buying age, fast-growing rents will fuel persistence in home shopping.

For persistent shoppers, shifting market conditions may make this fall–typically one of the best times of the year to buy a home–a particularly opportune one.

Home Sellers Face More Competition, but Seller-Buyers Get More Options

Homeowners continue to be in an advantageous position, especially those who have owned for longer periods of time and accumulated significant equity in their homes. This is likely to bring out more sellers hoping to capitalize on favorable market conditions which will ultimately mean more competition and a re-balancing of the housing market away from the very seller-friendly tilt it has recently had. This will bode particularly well for seller-buyers who have been more frustrated with the lack of buying options.

Seller-buyers are not immune from the challenges all buyers face, such as higher home prices and mortgage rates, but home equity insulates them from some of the impact, particularly those who have lived in their homes for a longer period. With more equity to leverage in a home purchase, seller-buyers can make a larger downpayment, minimizing the amount they borrow and taking some of the sting out of higher mortgage rates. This year, the return of seasonal trends and timing of mortgage rate increases are reinforcing each other, and I expect the market will cool off notably as we move toward the end of the year. This means that homeowners contemplating a sale should consider acting sooner rather than later. Another key takeaway in a transitioning market is that potential sellers need to be plugged into the latest market information and not let their expectations be too swayed by the past. While recent sellers have indeed benefitted from competitive market conditions, often selling quickly to buyers willing to waive contingencies and even pay more than asking price, even in this hotly competitive market some sellers–roughly 1 in 5–experienced offers falling through, and even a lack of buyers at the preferred price point. In fact, while the share of sellers having to reduce their asking price to find a buyer remains lower than pre-pandemic, it rose from one year ago in March, April, and May.

Subscribe to our mailing list to receive monthly updates and notifications on the latest data and research.